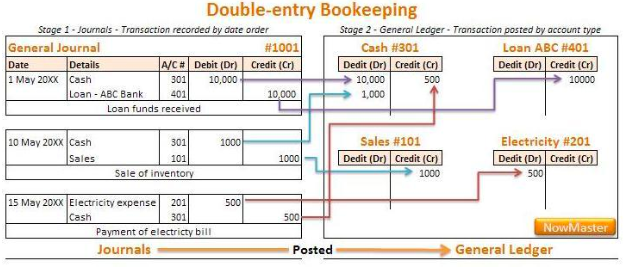

According to this system every business transaction affects at least two accounts in opposite directions. For example, if the furniture is purchased in the business, furniture is increased whereas the cash is decreased. There can be no transaction in the business which affects only one account or which has only one aspects.

Principles of Double Entry System-

(i) Every business transaction affects two accounts.

(ii) Recording of both personal and impersonal aspects.

(iii) Recording is made according to certain specified rules.

(iv) Preparation of Trial Balance.

Classification of Accounts-

Personal Accounts:

The accounts which relate to an individual, firm, company or an institution are called personal accounts. Account of Mohan, Account of Ram Chander Krishan Chander, Account of D.C.M. Limited, Account of Delhi University, Bank Account, Capital Account of the proprietor, Drawings Account of the proprietor etc. are examples of Personal Accounts.

Rule:

Rule for recording a transaction in personal accounts in simple words is ''Debit the receiver and credit the giver'. In other words, ''Debit that person's account who receives something from the business and credit that person's account who gives something to the business.

(A) Natural Personal Accounts-

Accounts of ‘Natural Persons’ means the accounts of human beings. For example, Mohan’s account, Sohan’s account, Seema’s account, Nirmala’s account etc. Proprietor capital account, Proprietor’s Drawings Account, Debtors Accounts and Creditors Accounts are also included in this category.

(B) Artificial Personal Accounts-

These accounts do not have physical existence as human beings but they work as personal accounts. For example, any Firm’s account, any limited company’s account, any institution’s account and any bank’s account and any bank’s account. These are treated as artificial persons for the recording of business.

(C) Representative Personal accounts-

When an account represents a particular person or group of persons, it is termed as a representative personal account. Examples of the Representative Personal Accounts are, Prepaid Insurance Account, Accrued Interest Account and Unearned commission account etc.

Real Accounts:

The accounts of all those things whose value can be measured in terms of money and which are properties of the business are termed as Real accounts, Such as cash accounts, Furniture account, Machinery account, Building account, Goodwill Account etc.

Rule-

Rule for recording a transaction in real accounts is 'Debit what comes in and credit what goes out'.Nominal Accounts:

These accounts include the accounts of all expenses and incomes.

The examples of nominal accounts relating to expenses are Salaries paid, Rent Paid, Discount allowed, Bad Debts etc.