A balance sheet is a financial statement that reports a company’s assets, liabilities and shareholders’ equity. The balance sheet is a snapshot, representing the state of a company’s finances (what it owns and owes) as of the date of publication.

PURPOSE:

The purpose of a balance sheet is to give interested parties an idea of the company’s financial position, in addition to displaying what the company owns and owes. It is important that all investors know how to use, analyze and read a balance sheet. A balance sheet may give insight or reason to invest in a stock.

GROUPING:

Grouping of Balance Sheet means putting items of similar nature under a common heading. accounting balance sheets classify a company’s assets and liabilities into distinctive groupings such as Current Assets; Property, Plant, and Equipment; Current Liabilities; etc.

MARSHALLING OF ASSETS AND LIABILITIES:

Marshalling of Balance Sheet means arranging the assets and liabilities in a particular order, i.e., in order of permanence or in order of liquidity.

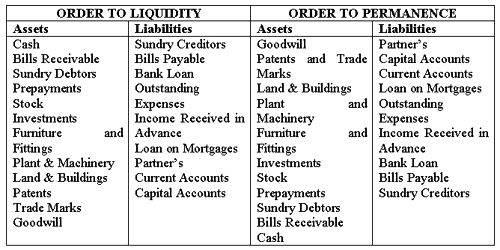

a) In order of liquidity:

Liquidity means convertability into cash. Assets will be said to be liquid if it can be converted into cash easily, they are placed at the top of the balance sheet. Liabilities are arranged in the order of their urgency of payment. The most urgent payment to be made is listed at the top of the balance sheet.

b) In order of permanence:

This order is exactly the reverse of the above. Assets and liabilities are recorded in the order of their life in the business concern.